Budgeting can be an intimidating concept, but it’s really nothing more than a plan for managing your income and expenses. Eighty percent of Americans follow a budget, according to a recent Debt.com survey. What’s more, the majority of folks in this camp say that budgeting has helped them stay out of debt.

The key is choosing a simple budgeting method that’s designed to prevent overspending. The 50/30/20 rule is just that. Here’s how to use it to build a strong financial foundation.

1. Clarify your income and expenses.

The 50/30/20 rule divides your spending into three main categories: essential expenses, discretionary spending, and financial goals. In order to do this, you’ll first need to take an honest look at your income and expenses.

- Your income

Think about any money you have coming in on a regular basis. This includes paychecks, as well as cash from any side hustles or part-time gigs. In a typical month, how much income are you generating? If your income fluctuates from month to month, that’s ok. You can look back over the last six months or so to get a feel for your average income. (Lowballing this number is a smart way to play it safe.) - Your expenses

Take the time to skim through your debit and credit card statements from the last few months. Now ask yourself how much you spend in an average month. You may notice a gap between what you think you’re spending versus how much you actually spend. If you’re overspending, take heart in knowing that you’re not alone — 17% of Americans spend more than they make, according to a 2020 report from the Financial Health Network. The good news is that understanding your spending habits can help you take control of your finances and establish new patterns.

2. Divide your expenses into different categories.

When reviewing your expenses, you’ll likely notice that they fall into one of the three main categories we mentioned earlier.

- Essential expenses

These are fixed expenses that you can’t really avoid — think rent or mortgage payments, utility bills, phone bills and so on. In other words, it’s regular monthly spending that’s related to your basic living needs. This includes regular debt payments like credit card minimum payments and student loan bills. - Discretionary spending

This type of spending isn’t technically essential, but it probably plays heavily into your lifestyle. This bucket refers to any expenses that make your life a little easier or simply bring you joy. Eating out, going to a concert, shopping with friends, grabbing coffee on the go; these are all examples of discretionary spending. - Financial goals

This refers to spending that’s related to your short- and long-term financial goals. Maybe you routinely set aside a certain dollar amount every month for your next vacation or the down payment on a house. If you’re kicking into a 401(k) or other type of retirement fund, these contributions go in this category.

It’s easy to get down on yourself if you feel like you aren’t putting enough of your income into this bucket. Think of it more as an opportunity to recognize your spending habits. It’s the first step in resetting your perspective so that you can start fresh and make real movement on your financial goals.

3. Take stock of where you are.

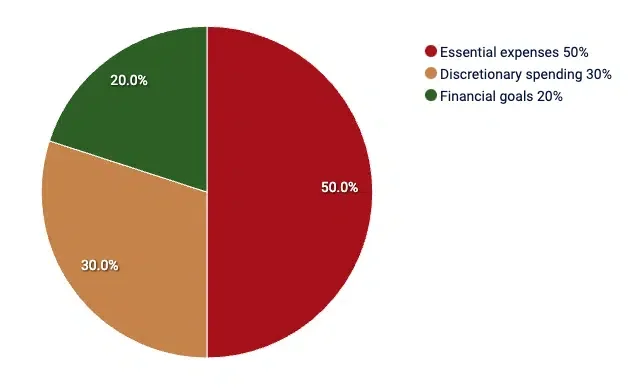

Now that you’ve clarified your spending, it’s time to add up the totals for each category. When you do the math, what percentage of your monthly income is being spent in each one. The 50/30/20 rule suggests dividing your spending like this:

If your current numbers don’t line up with these recommendations, don’t stress. You can now get intentional about making important tweaks.

4. Adjust your spending plan.

Reviewing your expenses might have made you realize that you’ve been overspending in certain categories. You can address these imbalances in the following ways:

- Swap out expenses

Let’s say your essential expenses are higher than you’d like so you’re not able to contribute enough to your financial goals. Is it possible to bring down your discretionary spending to make up the difference? Something as simple as meal planning and reducing your take-out orders could be enough to balance things out. - Reduce spending in each category

Even if your spending is on point for each category, bringing down your expenses can free up more money each month. You may have already spotted some budget-busters you can eliminate, like subscriptions you’ve been meaning to cancel or a cable bill you could easily live without. Calling your service providers and asking for rate reductions is another option. In fact, 69% of people who asked their credit card issuer for a lower interest rate ended up getting it, according to a CreditCards.com survey. Refinancing student loans or consolidating debt can also be effective. - Increase your income

If your spending is already pretty lean, making even deeper cuts could negatively impact your quality of life. Instead, look at your income. Is it possible to dial up your earnings? Picking up a side gig could tip the scales so that your budget is more livable. You might also consider approaching your employer for a raise if it’s warranted, or looking for a new job altogether. Don’t be afraid to think outside the box. Taking on a roommate or selling your car and opting for public transportation are larger-scale strategies that could transform your budget.

The 50/30/20 rule is a budgeting style that can set the stage for financial freedom. Treat it less like a hard-and-fast rule and more as a way to prevent overspending so that you can live comfortably and reach your financial goals. DailyPay is aligned with this vision and can help you make the most of your income.